Pixar Pitch

Once upon a time mergers and acqusitions (M&A) in many high tech firms was stratified as a financial transaction both in Wall Street and in cherry-picked Silicon Valley zipcodes. As a result, human capital was largely ignored like Cindrella, a drudge-like creature in the Technology Policy Ball. And because of that humanity seemed to be outside the radar of the human resources department. And because of that there was a slump in productivity and a majority of the workers were dissatisfied with their sense of accomplishment at work (also confirmed in Gallup polls). The prevailing conventional wisdom at the CEO and board levels staunchly believed that an adhoc mixture of one or more luck events, charismatic leadership and targeted rightsizing is the silver bullet for post-merger integration success. And because of that the strategic agility of the firm remained inherently weak and the accruing technical debt in the financially significant systems became a critical business issue (a three headed hydra) for the firm. Project management was also regarded an overhead which created a roadblock for the PMO to get a seat at the table. Until one day a grassroots campaign in the IT community to embrace the principles of the Agile Manifesto started a global movement in the business community to bring individuals and intereactions front and center as first class citizens, reject the tired traditions of yesteryear, adopt a system view and relentlessly focus on optimizing the business. As a result of this mandate, there was a visible change in priorities in the board room. And from that day forward, self-organizing teams catapulted into action by internalizing the founder’s touch and (1) welcomed the initial state of dissonance during post-merger integration to innovate, (2) built the muscle of strategic agility at scale in the enterprise and (3) revived the passion for Managing by Wandering Around (MBWA).

Context

What is the M&A situation?

Nokia was a platform-based acquisition with a complexity that metaphorically represented a reverse two and-a-half somersault with a half twist. The acquisition, classified as a “burning platform,” was originally intended to provide a center of gravity for Microsoft to make an entry in the mobile phone business. As a challenger, this presented an opportunity to make a radical change to navigate towards uncharted waters in terms of both the upstream and downstream parts of the value chain while retaining existing and acquiring new Nokia customers.

“Nokia, our platform is burning.”

“We are working on a path forward — a path to rebuild our market leadership. When we share the new strategy on February 11, it will be a huge effort to transform our company. But, I believe that together, we can face the challenges ahead of us. Together, we can choose to define our future.”

“The burning platform, upon which the man found himself, caused the man to shift his behavior, and take a bold and brave step into an uncertain future. He was able to tell his story. Now, we have a great opportunity to do the same.”

Dated: Feb 9, 2011

At that time, as a shareowner, I had an outside in perspective of the firm and presented a compelling, not-to-miss opportunity to create a cadre of Activist Turnaround Managers (ATM, pun intended) on Main Street. I published a blog post in February 2011.

The corporate renewal of Nokia was not successful. The bad news was communicated via the “Hello There” memo.

“Companies spend more than $2 trillion on acquisitions every year. Yet study after study puts the failure rate of mergers and acquisitions somewhere between 70% and 90%.”

Clayton Christensen, The M&A Playbook, Harvard Business Review, Jul 2015

Precision Question

How do we turnaround the context from a public narrative of a high-visibility face-plant to write-off a failed acquisition as a distressed asset in the balance sheet to one that is more solution focused (SF), hands on, which also strikes a chord with both the financial and human propositions to achieve post-merger integration success?

Learning from Jack Welch

At an April 1986 board meeting in Kansas City, I had argued for it – and unanimously swung the board my way. It was a classic case of hubris. Flush from the success of our acquisition of RCA in 1985 and Employers Reinsurance in 1984, I was on a roll. Frankly I was just full of myself. While internally I was still searching for the right “feel” for the company, on the acquisitions front I thought I could make anything work. There’s only a razor’s edge between self-confidence and hubris. This time hubris had won and taught me a lesson I’d never forget. The Kidder experience never left me. Culture does count, big time.

(Jack Welch, Straight from the Gut, 2001)

“Even so, as lessons go, $7.5 billion is pretty steep tuition.“

Hindsight is always 20/20. Rather than fall into the conventional trap of casting the blame on an individual for a bad deal (“tire that had a flat”), in a solutions focused (SF) approach we avoid spending an inordinate amount of time to find out why it is flat (root cause analysis) and focus instead on getting a new tire to try to make sure it stays inflated (i.e., make a good deal better and avoid a bad deal — sage advice that I learned at Ernst & Young). Jack Welch’s insights also emphasizes the importance of human capital during post-merger integration. However, the venture integration group in most firms often fall into the trap of viewing a potential acquisition only through a financial lens and worry less about the heavy lifting required during post-merger integration.

The Nokia acquisition was probably originally intended to be an enhancement deal since it was designed to bring the acquirer capabilities that it didn’t yet have but would allow it to intensify its own capabilities system. However, studies have shown that unlike leverage deals, both enhancement deals and limited-fit deals don’t produce the best returns.

M&A deals continue unabated

The 15 Biggest M&A Deals Of 2015 (so far) consist of the following:

- Private equity firm Thoma Bravo and the Ontario Teachers’ Pension Plan completed the acquisition of Riverbed Technology for approximately $3.5 billion.

- Sopos acquired SMB email security and archiving company Reflexion Networks for an undisclosed account.

- DLT Solutions was was acquired by private equity firm Millstein & Co. for an undisclosed amount.

- HP bought Aruba Networks for $3 billion.

- Bain Capital acquired security firm Blue Coat Systems for $2.4 billion.

- PCM acquired solution provider and systems integrator En Pointe Technologies for $15 million. (En Pointe is one of Microsoft’s largest licensing solution providers in the country.)

- Nokia acquired French rival Alcatel-Lucent for $16.6 billion.

- Fortinet acquired Meru Networks in a deal valued at approximately $44 million.

- Cisco acquired OpenStack specialist Piston Cloud Computing to accelerate its Intercloud strategy. (undisclosed amount)

- EMC acquired cloud computing company Virtustream for $1.2 billion.

- Accuvant and FishNet have completed their merger and will launch as Optiv Security.

- SofwareOne acquired the software licensing business of $2.2 billion solution provider CompuCom.

- Intel acquired semiconductor manufacturer Altera for $16.7 billion to bolster its Internet of Things business.

- Avago is buying rival Broadcom in a $37 billion deal.

- Charter Communications is purchasing of Time Warner Cable for $56 billion as well as buying Bright House Networks for $10.4 billion.

Post-merger integration success is not guaranteed for all the above deals. While there is no universal recipe, I feel that it is a valuable exercise to explore some options to “make a good deal better and avoid a bad deal.”

Higher Intent

One level up

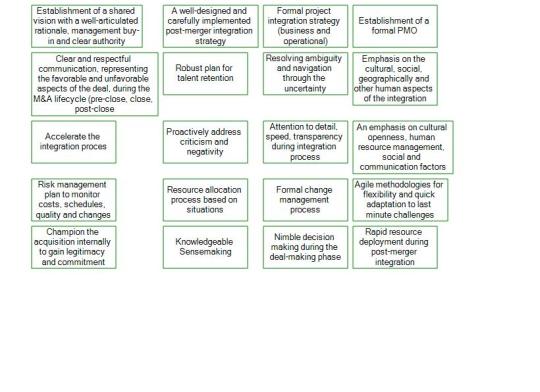

The following Post It notes represent a subset of undesirable effects (UDEs) during an unsuccessful post-merger integration.

The higher intent “one level up” (my boss) is to reverse the UDEs and achieve a large subset of the following outcomes during the post-merger integration of a firm.

Two levels up

Taking an ounce of Tom Peters’ sage advice, the leadership (two levels up) has a recognized that a culture of execution-accountability is a pre-requisite for achieving corporate renewal (inclusive of situations during post-merger integration). Aside from the size of the deal, at a tactical level, execution excellence requires leaders to re-learn the behavior of Managing by Wandering Around (MBWA), which was the rhythm of the business during a bygone era at Hewlett-Packard (now in distant memory).

My Intent as a Shareowner

What are we trying to achieve and why?

What

- Reframe past M&A failures as “fallure“ so that organizational leaders can learn to adopt a growth mindset in a turbulent environment

- Use the M&A (both pre- and post-merger) as a springboard to develop the generative process for strategic agility of the firm. (click on the link to view the dialogue map)

- Develop the capability to notice an opportunity and make a rapid yet precise move using extraordinary accelerating power

- Develop the capacity of making knowledgeable, nimble, rapid strategic moves with a high level of precision

In order to

- Improve sensemaking, decision making and resource deployment during the selection, acquisition and integration phases of a merger

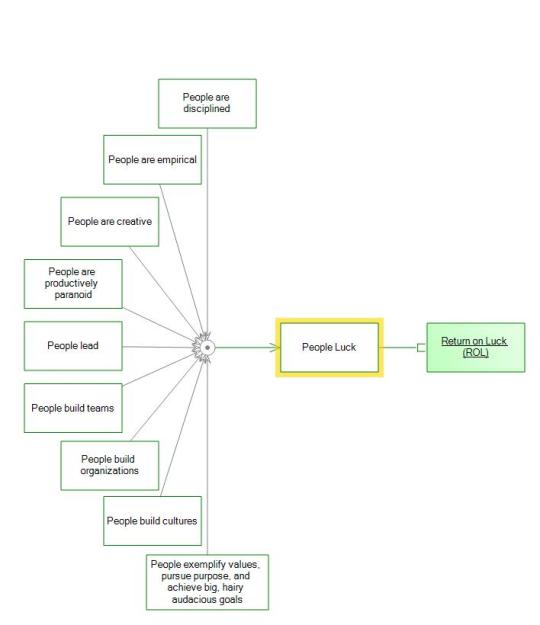

- Increase Return on Luck (ROL) during post-merger integration and build a relevant @ResponsiveOrg

Rationale

A longitudinal panel of over 400 observations across multiple firms and industries has revealed that post-merger success hinges on achieving the dual goal of simultaneously improving customer satisfaction and operational efficiency. This in turn enables the merger to achieve a significant increase in long-term financial performance.

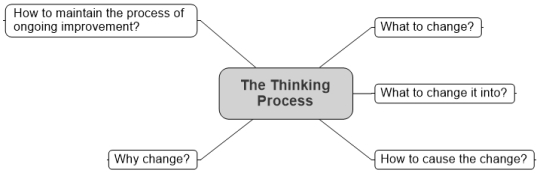

A lack of systems thinking during post merger integration can cause corporate myopia. We urge that one has to think outside the box, understand the causality among the undesirable effects (identified earlier) and target what to change, where to change and how to change.

Digital business strategy extends the scope beyond firm boundaries and supply chains to dynamic ecosystems that cross traditional industry boundaries. A digital firm’s design capital is the cumulative stock of designs owned or controlled by a firm. Design capital is a fundamental construct to the emerging logic of digital business transformation. The salient dimensions of design capital are option value and technical debt. In order to be strongly positioned for innovation and platform leadership, high-quality design capital is characterized by high option value and low technical debt. A study by the UK Design Council in 2005 revealed that companies with a sustained track record in design outperformed their peers in the FTSE 100 over a 10-year period by a startling 231 percent.

Akin to fiscal debt, technical debt is a common occurrence during systems development where time pressures or resource constraints cause developers to take shortcuts. Left unmonitored, accumulating technical debt obligations causes the cost of quality to increase over time which in turn impacts customer satisfaction and revenue generation.

In a radical departure from earlier efforts, we have realized that during post-merger integration, it is vital to proactively manage the design capital of the firm (in addition to the firm’s balance sheet) by monitoring and controlling both technical debt.

Operationalizing strategic agility in an enterprise

Disciplined Agile is a process decision framework for a digital business at an enterprise level. Pioneered by Scott Ambler and Mark Lines, Disciplined Agile recognizes that an organization is a complex and adaptive system. Moreover, it is unrealistic to impose a “one-size-fits-all” agile-in-the-large model in a (global) enterprise.

Based on the cumulative real-world experiences from several hundred IT projects, Disciplined Agile is a proven framework for an enterprise to grow the muscle of strategic agility at scale in both IT and non-IT situations. Disciplined Agile has a rigorous focus on (1) the iterative delivery of consumable solutions (business value), (2) continuous learning from retrospectives, and (3) fostering an agile mindset around the enterprise. By adopting Disciplined Agile, leaders can achieve the following:

- Pay increased attention to the (soft) human, cultural and non-functional deal aspects

- Diminish the impacts of unknown elements (risk/value tradeoff) using an iterative incremental manner

- Actively optimize technical debt and increase the design capital of the firm

Recognizing that there are several cross-project dependencies during any post-merger integration, there will typically be an active Project Management Office (PMO) that will be monitoring the project portfolio at an enterprise level. Disciplined Agile teams and PMO should work together and leverage suitable processes from PMBOK (Project Management Body of Knowledge) to practice project execution excellence.

The primary takeaway is that during post-merger integration, the secret sauce rests not on the framework per se but, echoing Tom Peters’ words, a culture of execution-accountability and Managing By Wandering Around (MBWA) in the trenches during post-merger integration. The Activist PMO Leader walks the Disciplined Agile talk with a learning by doing perspective and co-creates the generative process of strategic agility of the firm.

Boundaries

Freedoms

- In order to build a resilient organization, establish self-organizing teams that practice autonomy, mastery and purpose.

- Harness a culture of innovation so that the firm can become more intrapreneurial

Constraints

- According to Barry Boehm, a system will succeed if and only if it makes winners of its success-critical stakeholders. This implies the importance of stakeholder management during post-merger integration.

- Adopt the lean principle and minimize waste during post-merger integration.

- Proactively identify the weakest link in the value chain during post-merger integration. This is a continuous activity (not just once at inception).

Backbrief

Has the situation changed?

The retrospectives from each of the projects in enterprise project portfolio creates a force multiplier for the firm to be in a state of continuous improvement and actively track the health of the human capital, the value of the design capital and the financial performance.

Sendoff

Playing devil’s advocate, it is reasonable to critique that our proposal for post-merger integration success is either an unproven idea or old wine in new bottles. That said, the core tenet is to build the muscle of strategic agility and a passion for Managing by Wandering Around (MBWA) during the post-merger integration journey.

References

- Patel, R., “Applying Project Management Approaches to Achieve Value Creation in Post -Acquisition Integration”, The ISM Journal of International Business, ISSN 2150-1076, Volume 1, Issue 4, October 2012.

Such a frame of reference symbolized a powerful moment of truth for leading by example and, if successful, could become a legend for the current and future generations. The Spirit of MLK ignored the conventional wisdom of the balance sheet view of the firm and avoided falling into the trap of mining its deficits and denominator-based management (arbitrary corporate downsizing). By employing a reframed lens that “corporations are [made up of] people” and a business is a portfolio of projects, the Spirit of MLK creatively explored how to revitalize the distressed asset by nurturing its body and soul and increasing employee engagement and accelerate value creation. The Spirit of MLK clearly understood that inside every distressed asset is a diamond in the rough (I.e., increase throughput, decrease inventory, decrease operating expenses). The Spirit of MLK brainstormed using the following questions:

Such a frame of reference symbolized a powerful moment of truth for leading by example and, if successful, could become a legend for the current and future generations. The Spirit of MLK ignored the conventional wisdom of the balance sheet view of the firm and avoided falling into the trap of mining its deficits and denominator-based management (arbitrary corporate downsizing). By employing a reframed lens that “corporations are [made up of] people” and a business is a portfolio of projects, the Spirit of MLK creatively explored how to revitalize the distressed asset by nurturing its body and soul and increasing employee engagement and accelerate value creation. The Spirit of MLK clearly understood that inside every distressed asset is a diamond in the rough (I.e., increase throughput, decrease inventory, decrease operating expenses). The Spirit of MLK brainstormed using the following questions:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Recent Comments